-min.webp)

Veronica’s Journey: Balancing Law School, Crypto Freelancing & Cross-Border Payments

This post is based on an interview we conducted with Veronica in March 2025.

Money Moves is a series in which we interview MiniPay users from all walks of life about their personal finance situation. The views expressed are solely those of the interviewees, based on their personal experiences – as such they should not be considered financial advice or MiniPay's views.

We have changed the name of the interviewee for their privacy.

Hi Veronica! Let’s start with a simple one: who are you, and what do you do?

I’m Veronica – 21, currently living in Lagos, Nigeria. I’m a final year law student at the University of Lagos, but I also write content for crypto startups on the side. Oh, and I try to squeeze in Netflix where I can, because, you know, self-care lol.

Breaking into the crypto industry

Veronica, how did you end up writing for a crypto company while still in university?

Well, I started writing in my first year as a ghost writer for a friend, and soon enough I saw an online job ad for content writers with tech/finance experience. I knew nothing about cryptocurrency then, but they liked my writing samples and gave me a shot. My first assignment was on yield farming, which was not entry level crypto knowledge at all. Over time, I learned a lot through lots and lots of research.

Getting paid in USDT: the process

So you’re paid in USDT. How does that actually work?

My company pays me every month into our centralized wallet. But the path to actual spendable cash looked more like this:

- Salary is paid into the company’s custodial wallet

- Withdrawal Rate Dilemma – The exchange rates in the wallet are often very poor – often 20-30% below market, and sometimes there just aren’t any offers available.

- So I used to send it to Binance (when it was still an option).

- Most times, I would leave the cash in USDT and only withdraw or convert what I needed, or just waited for a better rate

- Sometimes I’m also forced to change in bits because of daily transaction caps that can block big transfers.

"At some point, I felt like a microfinance bank, juggling multiple apps just to move my own money"

-min.webp)

Balancing law school and freelance writing

You mentioned being a full-time student. What’s your schedule like?

I’m usually up by 7 or 8 AM. I’ll do some writing or editing for a few hours. After that, I have classes or study groups. I come back, maybe write more if I’m not too tired, watch a Netflix show or two, then pass out. Rinse and repeat. If I’m in exam season, it’s way worse – sometimes I don’t write at all and outsource my workload to friends who help me out.

Outsource? That’s interesting. So you’re kind of an unofficial project manager too?

Haha, basically! I realised early on that I couldn’t handle everything alone. I found other writers who are just as good and started delegating tasks to them during my busiest weeks. But managing that also means I have to handle multiple payments – sending them their cut, making sure the exchange rate doesn’t eat me alive, and so on.

Get paid in dollars. Withdraw instantly.

MiniPay lets you receive stablecoins like USDT and withdraw to local currency instantly—with zero fees.*

Income & budget breakdown

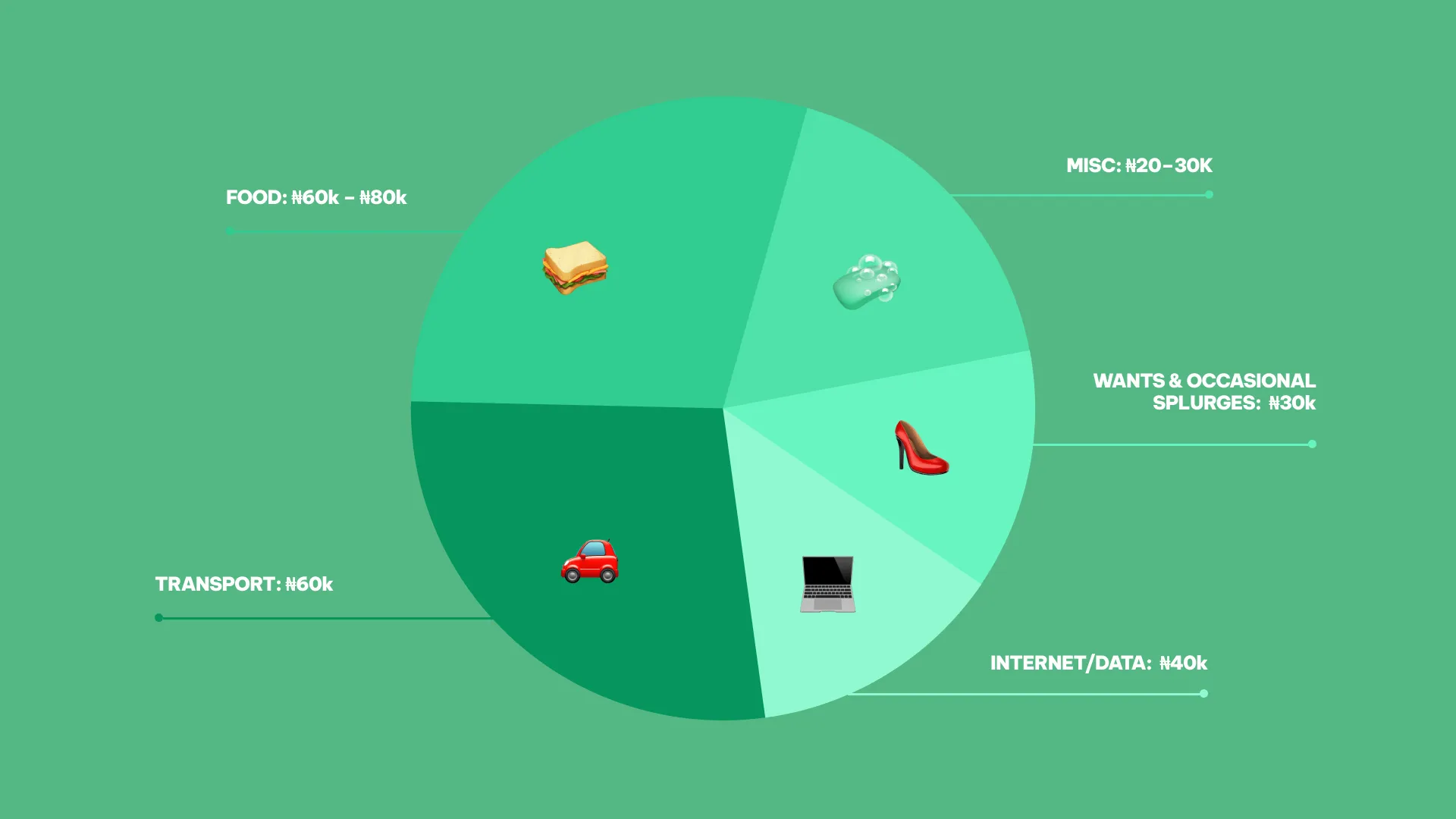

Can you give us a rough idea of what your monthly spending looks in actual amounts?

Sure. In local currency, I’d say my total personal monthly spend is around ₦200,000 (give or take). That covers:

- Food: If I cook regularly, maybe ₦10k a week. If I’m eating out a lot (especially during exams), it can jump to ₦20k or ₦25k a week. So that’s anywhere from ₦80k to ₦100k a month on food.

- Transport: Around campus, it’s pretty cheap – like ₦5k a week. But I travel to church far away once a week, which can be about ₦10k each Sunday. So total transport can hit ₦15k–₦20k, plus an extra ₦40k a month if I’m going to church weekly. Sometimes I carpool, so it’s less.

- Internet/Data: Easily ₦40k a month – I’m a freelancer, so I can’t skimp on data.

- Wants & Occasional Splurges: Maybe ₦30k on clothes or accessories once in a while.

- Misc. (books, hygiene items, Sunday food shopping): Another ₦30-50k or so monthly.

That’s roughly how it goes, but it fluctuates with my schedule and whether I’m more of a “cook at home” or “eat out” person that month.

Dealing with multiple apps

It sounds like you juggle a lot of apps – crypto wallets, local bank apps, etc. Is that a hassle?

Oh, absolutely. I wish I could keep everything in one place, but I need each one for a different reason. Here’s my current lineup:

- Bank App: For basic bills and mainly the debit card for in-person payments.

- Mobile wallet: Less formal and more used because my bank app has a transaction limit.

- Savings App: with forced/automated savings features so I don’t finish all my money.

- Crypto Exchange Wallet: Where I actually receive my USDT salary.

- Investment App (like Bamboo): For stocks/ETFs.

- MiniPay: This has replaced a few of the above because I can just send my USDT here and use it straight away whether online or for in-person purchases.

"It's ridiculous, but you need backups. One day your favourite app might just say Nope. Not today, leaving you stranded"

If you could build your dream financial app, what features would it have?

- Savings & Spend tracker: Let me see my savings in one place.

- Automated Savings: Direct debits and the ability to “lock” my savings away automatically.

- No Strict Transaction Limits: I don’t want to have to beg a bank manager to raise my daily cap.

- Easy USD- Local Currency Swaps: Let me spend or send USD directly if I want, or convert only when I choose.

- Simple UI: I’m tech-savvy, but clunky apps kill me. Make it user-friendly!

Veronica’s payment graveyard

Being a remote worker, you’ve probably tested multiple international payment methods. What’s your verdict?

It’s almost comical how many services I’ve tested:

- Upwork: High fees (15–30%). One time I earned $50, but only $35 actually reached me. I felt like I was paying for the privilege of working!

- PayPal: Inbound payments are not allowed. in my country. I couldn’t receive money at all, so that was dead on arrival..

- Wise: Stopped servicing my country, so another door slammed shut.

- Domiciliary Account (USD Bank Account): After jumping through hoops, finding people to stand in as referrals just to open the account, I found out that I actually can’t withdraw without a dollar card. I still haven’t had time to go figure that one out

- Various Crypto Exchanges (Binance, etc.): Region blocks. Binance stopped operations locally, and I lost some money I had left in my wallet – which is kind of funny but also not funny at all. At the moment, you can’t even open Binance’s website without a VPN, to say nothing of using the app.

System upgrades & blocked wallets

Which experience really pushed you to the edge?

In one instance, I tried withdrawing ₦300k in USDT using P2P on another popular crypto wallet to my local bank, and it took 10 days before I received the money because the bank was having some “system upgrade.” I nearly pulled my hair out. I had to pay my freelance teammates from my personal savings while waiting. It’s stuff like this that makes me want to keep my money in stablecoins. At least I know it won’t vanish into some bank black hole.

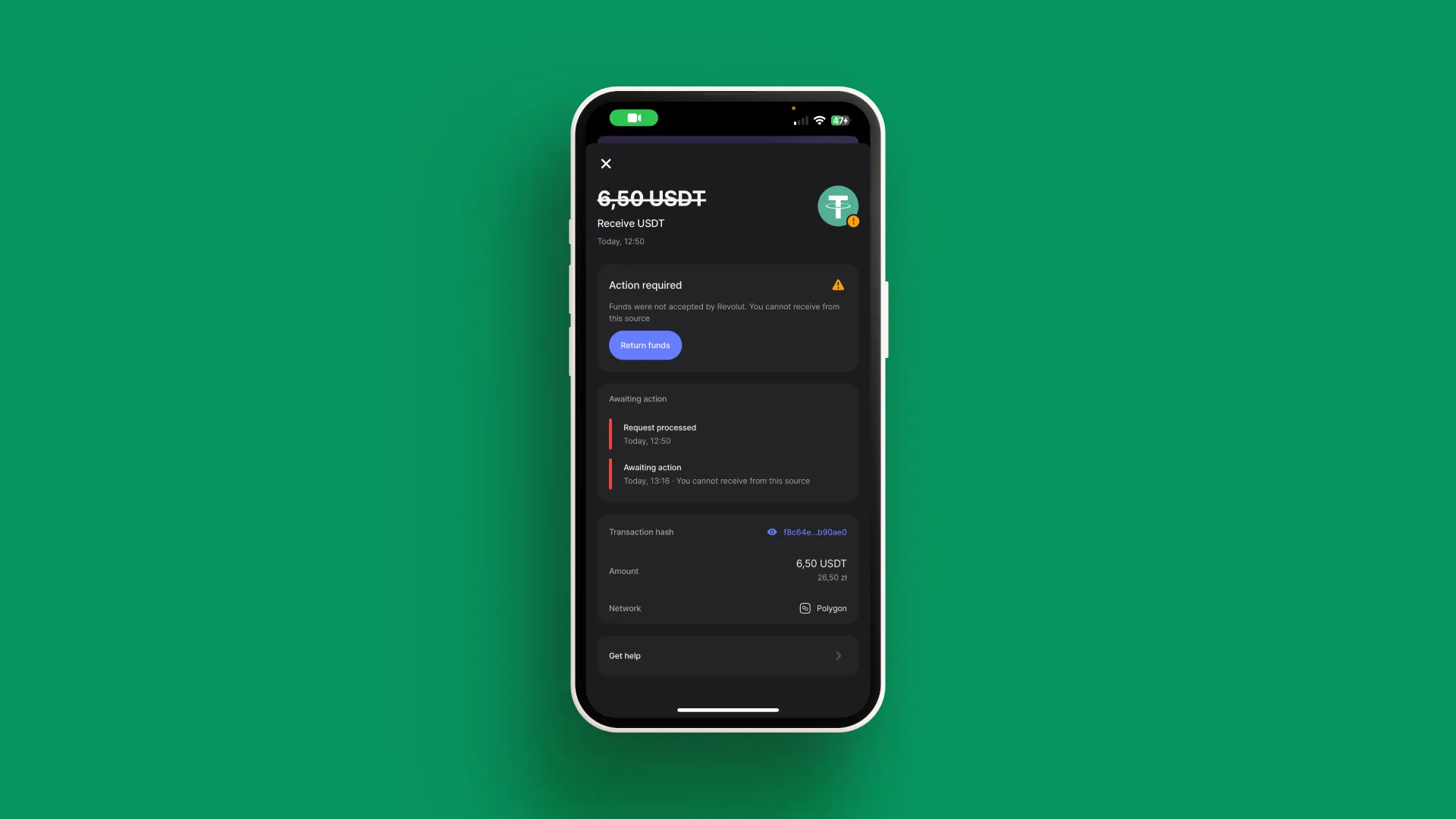

One time I was trying to send money to my sister in Europe. I thought I had figured out a solid way to do it – USDT to her Revolut wallet. Smart, right? WRONG. Turns out Revolut was like, ‘We don’t know that person.’ The money got sent back, and I was there, holding my head, stressed and confused.

"I kept thinking it's no longer about having money, because even when you have it, you can't move it or spend it"

Discovering a smoother way to spend USDT locally

So how did you stumble on MiniPay?

When I first heard about MiniPay, I just used it as an easier place to hold my USDT earnings. But then, the first time I used it to withdraw, the experience was so much smoother than the horrors I had faced with P2P platforms. Then I realized I could pay directly in local currency for groceries and all without needing to cash out. Not only are the rates so good, but it’s also fast and reliable. One time the funds actually took more than a few seconds to show up, but I had no doubt in my mind the issue was with the receiving bank because MiniPay has never failed me before.

What makes MiniPay stand out to you?

Simplicity. It’s easier than other wallets I’ve tried. And then spending in USD: No need to swap to local currency first. That’s a real game changer

Get paid in dollars. Withdraw instantly.

MiniPay lets you receive stablecoins like USDT and withdraw to local currency instantly—with zero fees.*

Do you have a story? We’d love to hear it. Share your experiences with interacting with crypto and stablecoins, sending money internationally, managing multiple apps, or any hacks you’ve discovered. Because when it comes to making and moving money, we’re all learning – one transaction at a time.

.webp)